For millions of Americans, Medicare enrollment is not a one-time event but a process punctuated by specific life changes and deadlines. Understanding what triggers Medicare enrollment inquiries is crucial for both beneficiaries navigating the system and professionals guiding them. These triggers are the pivotal moments when individuals transition from passive awareness to active research, seeking clarity and actionable steps. This article explores the major catalysts that prompt people to ask questions, seek help, and ultimately make critical decisions about their healthcare coverage.

Initial Eligibility: The First Major Trigger

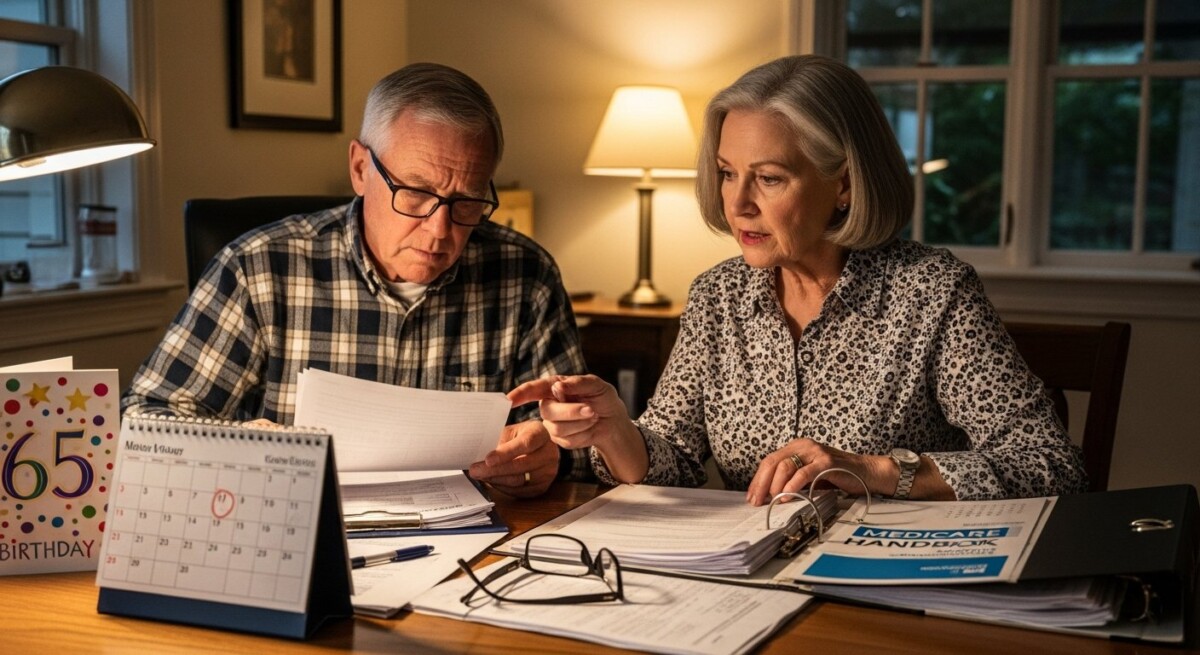

The most common and predictable trigger for Medicare enrollment inquiries is approaching the age of 65. This milestone generates a flood of questions as individuals, often still employed or covered under a spouse’s plan, must decipher a complex new system. The inquiry process typically begins several months before their 65th birthday month. People want to understand the difference between Medicare Part A and Part B, whether they should enroll automatically or need to sign up, and the consequences of delaying if they have other coverage. The looming Initial Enrollment Period (IEP), a seven-month window surrounding their birthday month, creates a tangible deadline that spurs action. This initial trigger is foundational, setting the stage for all future Medicare-related decisions.

Life-Changing Qualifying Events

Beyond age, significant life events create Special Enrollment Periods (SEPs), which are powerful triggers for urgent enrollment inquiries. These events change a person’s healthcare coverage landscape abruptly, necessitating quick research and action.

Employment Status Changes

Leaving a job that provided health insurance after age 65 is a major trigger. Individuals who delayed Medicare Part B because they had employer-sponsored coverage now face a critical decision window. They must navigate the rules for their eight-month Special Enrollment Period that begins the month after employment ends or the group health coverage ends, whichever happens first. Inquiries during this time are highly specific and time-sensitive, focusing on avoiding late enrollment penalties while ensuring no gap in coverage.

Loss of Other Credible Coverage

Similar to job loss, the loss of any qualifying coverage acts as a trigger. This could include the termination of COBRA coverage, the end of a spouse’s employer plan that provided family coverage, or a change in status under the Affordable Care Act marketplace. When other coverage disappears, Medicare becomes the primary option, prompting immediate inquiries about enrollment steps, effective dates, and plan selection. For a deeper look at options after a missed deadline, our resource on missed Medicare enrollment deadlines provides essential guidance.

The Annual Election Period and Plan Dissatisfaction

The Medicare Annual Election Period (AEP), which runs from October 15 to December 7 each year, is a massive, recurring trigger for enrollment inquiries. During this time, beneficiaries can switch between Original Medicare and Medicare Advantage, change Part D plans, or switch between Medicare Advantage plans. Inquiries peak as people evaluate their current plan’s performance over the past year. Common triggers within the AEP include:

- Significant premium or deductible increases for their current plan.

- Changes to the plan’s formulary (covered drug list) that affect their prescriptions.

- Their doctors or preferred hospitals leaving the plan’s network.

- Experiencing high out-of-pocket costs over the previous year and seeking better coverage.

- Simply wanting to explore new plan benefits or options that have entered the market.

This period is characterized by comparative research, with beneficiaries seeking help to analyze and understand the nuances of multiple plan options side-by-side.

Health Status and Financial Circumance Changes

A change in personal health or financial situation is a deeply personal trigger that often leads to private, urgent inquiries. A new chronic diagnosis, for instance, may make a Medicare Advantage Special Needs Plan (SNP) relevant or highlight the need for a more robust Part D plan. Conversely, a beneficiary experiencing financial strain may inquire about switching to a lower-premium plan or exploring Medicare Savings Programs. Other related triggers include qualifying for Medicaid (dual eligibility), which opens new plan options, or needing more comprehensive coverage like a Medicare Supplement (Medigap) plan after a serious health episode. These inquiries are less about calendar deadlines and more about adapting coverage to profoundly changed life circumstances.

Geographic Relocation

Moving to a new service area is a clear and practical trigger for Medicare enrollment inquiries. Medicare Advantage and Part D Prescription Drug Plans are location-specific. A beneficiary who moves outside their plan’s service area, or even to a new county within the same state, typically has a Special Enrollment Period to choose a new plan. Inquiries focus on which plans are available at their new address, how to ensure continuity of care with new providers, and the steps required to disenroll from their old plan and enroll in a new one. This trigger emphasizes the importance of local market knowledge in Medicare guidance.

Marketing and External Outreach

External stimuli directly trigger enrollment inquiries. Beneficiaries are inundated with marketing, especially during the AEP, through mailers, television advertisements, telemarketing calls, and online ads. A well-timed mailer or a conversation with a friend about their plan can prompt someone to question if they are in the right plan. Furthermore, outreach from trusted community sources, like senior centers, healthcare providers, or local State Health Insurance Assistance Programs (SHIP), raises awareness and triggers proactive inquiries. These external prompts often serve as the initial spark that leads an individual to seek more detailed, unbiased information.

Navigating Denials and Complex Situations

Sometimes, the trigger is a problem. A denied claim, an unexpected bill, or a confusing explanation of benefits (EOB) can lead to a reactive inquiry about whether their current enrollment or plan choice is the root cause. More seriously, receiving a notice of denial for Medicare enrollment itself is a high-stakes trigger that demands immediate action. Individuals in this situation need to understand their appeal rights and next steps. For those facing this challenge, our article on what to do if your Medicare enrollment is denied outlines the critical process to follow.

Frequently Asked Questions

What is the biggest mistake people make regarding enrollment triggers? The most common mistake is missing a Special Enrollment Period (SEP) deadline after a qualifying life event. Many assume they can enroll anytime after losing coverage, but SEPs have strict time limits, often 60 days. Missing this window can mean waiting for the General Enrollment Period and incurring late penalties.

Does retiring trigger a Medicare enrollment period if I’m already 65? Yes. If you delayed Part B (and possibly Part A) because you had employer coverage, your retirement and loss of that group health plan triggers an eight-month Special Enrollment Period to sign up for Medicare without penalty.

I’m turning 65 but have VA benefits. Does that trigger a need to enroll in Medicare? While VA benefits are excellent, they are not considered “creditable coverage” for Medicare purposes. Enrolling in Medicare Part B when first eligible is often recommended to avoid penalties and to provide coverage for non-VA providers. This specific scenario triggers complex inquiries best addressed with a professional who understands both systems.

Can a change in my income trigger a Medicare enrollment inquiry? Indirectly, yes. A change in income may make you eligible for programs like Extra Help (Low-Income Subsidy) for Part D or a Medicare Savings Program, which could trigger an inquiry into changing your Part D plan or overall strategy to reduce costs.

Where can I get a complete overview of the entire enrollment process? For a foundational understanding, reviewing a comprehensive guide to Medicare enrollment is an excellent first step to contextualize all these triggers.

Recognizing what triggers Medicare enrollment inquiries is the first step to providing timely, effective assistance. These triggers, whether calendar-driven or born from life’s unpredictability, represent critical inflection points in a person’s healthcare journey. By anticipating these moments and understanding the specific questions and concerns they generate, agents, advisors, and caregivers can offer proactive support. This transforms a reactive process into a guided, confident decision-making experience, ensuring beneficiaries secure the coverage they need precisely when they need it most.

{kind=link}

{kind=link}

{kind=link}

{kind=link}